Many involved in the Vancouver housing affordability discussion think the problem is that we aren’t building enough homes. They look at active listings — which are indeed low — and conclude we have a supply problem.

Last month, B.C. Finance Minister Mike de Jong said,

“I don’t believe the answer is to try and artificially constrain demand whether it is from within the country, within the province or internationally. I think the answer is for us to work together as governments and increase supply.”

On June 2, at the UDI Luncheon, Bob Rennie went as far as saying, “only supply will cool the market”.

Over on Twitter, urban development specialist Bob Ransford’s favourite hashtag is #ItsSupplyStupid.

Well, is it supply? Are we stupid?

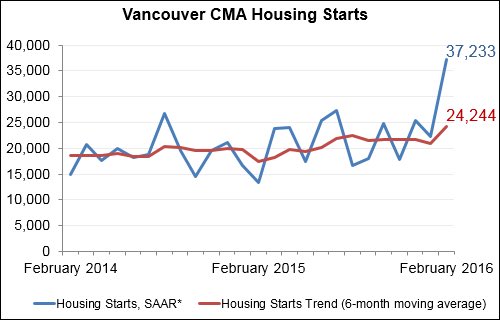

Here are the housing start numbers from CMHC. It certainly doesn’t look like a supply problem!

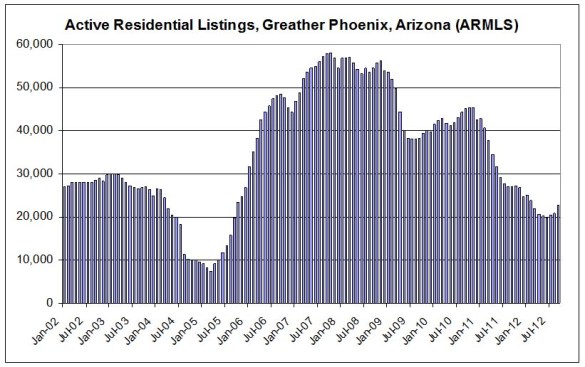

Maybe this supposed supply problem is really a demand problem? When housing markets are overheated, sellers are reluctant to sell and fence-sitters jump into the market because of their fear of missing out. Just look at what happened to supply in Phoenix in 2005 when their market went nuts. Inventory dropped to historic lows, from over 25,000 to under 10,000 in less than a year.

I’ll bet the Bob Rennies and Mike de Jongs of Phoenix were complaining about a supply problem too. But once the market slowed, look how fast supply magically appeared! From under 10,000 to over 40,000 in a year. That’s what happens when a market turns. Buyer’s fear of missing out turns into fear of losing money. And developers, thinking more supply is needed, ramp-up activity. As a result, sales numbers fall and inventory takes off.

What might have looked like a shortage was really excessive demand. Based on the housing start numbers, it’s reasonable to conclude the same is true today in Vancouver. Maybe it’s demand, stupid?